Indicadores

| Título del ítem | Sumario | Categorías | Creado | |

|---|---|---|---|---|

| Export: per il vino un nuovo record commerciale:7,9 miliardi di euro di euro (+9,8%) | AgronewsExport: per il vino un nuovo record commerciale:7,9 miliardi di euro di euro (+9,8%)E' quanto emerge da analisi dell’Osservatorio Uiv, Ismea e Vinitaly. Rallenta la crescita: nell’ultimo trimestre +4,8% valore e -3,2% volume

Roma- L’Italia del vino sfiora il traguardo degli 8 miliardi di euro chiudendo l’export 2022 con un nuovo record commerciale:7,9 miliardi di euro di euro (+9,8%) a fronte di volumi piatti (22 milioni di ettolitri, -0,6%). Secondo l’analisi dell’Osservatorio Uiv, Ismea e Vinitaly, che ha elaborato i dati rilasciati oggi da Istat sui 12 mesi dello scorso anno, il mercato ha retto anche alle inevitabili quanto parziali variazioni dei listini, ma l’escalation dei costi di produzione ha abbondantemente eroso i margini della filiera in particolare per i prodotti entry-level e popular (fino a 6 euro al litro). Il risultato finale, vista anche la congiuntura, è senz’altro positivo per uno dei settori del made in Italy più virtuosi nella bilancia commerciale, che chiude in attivo di oltre 7,3 miliardi di euro. Rimane, rileva l’Osservatorio, la consapevolezza che il record commerciale sia senz’altro determinato da un doping dei prezzi, tanto necessario al fine di limitare l’erosione dei margini causata dal surplus dei costi, quanto pericoloso sul fronte dei consumi previsti per il 2023. Ultimo trimestre in forte rallentamento, con chiusura nei valori a +5% contro +19% di marzo, +11% di giugno e +12% di settembre, mentre i volumi si mantengono in scia negativa (a -3% medio da giugno, con il solo primo trimestre positivo). Tra i competitor, la Francia si conferma leader mondiale con 12,3 miliardi di euro (+11% valore e -5% volume) mentre l’Italia mantiene la posizione di primo fornitore a livello quantitativo e secondo in valore davanti alla Spagna (2,98 miliardi di euro, che chiude a +3,5% nei valori e -9% nei volumi).

MERCATI Incrementano a valore tutti i principali mercati della domanda, a partire dagli Stati Uniti (+10%) che si confermano primo mercato export italiano con una quota di mercato del 23%. Seguono, tra i top buyer, la Germania (15% lo share), che sale del 5% a 1,2 miliardi di euro; poi Regno Unito (+10%), Canada (+11%), Svizzera (+3%) e una Francia in forte progressione (+25%). Diverso il quadro dei volumi, in calo o stazionari in tutte le principali destinazioni (Usa a -6%, Germania a -2%, Uk a -4%) a eccezione di quella transalpina (+16%, dovuto alla poderosa crescita del Prosecco, +20%). Ancora in caduta la domanda cinese, che chiude i conti a -28% sul fronte dei vini in bottiglia.

TIPOLOGIE Tra le tipologie – rileva l’Osservatorio targato Unione italiana vini, Ismea - Istituto di servizi per il mercato agricolo alimentare e di Vinitaly – continua il forte traino degli spumanti che volano a +19% in valore (Prosecco a +22%) e confermano la positività sui volumi (+6%, di cui +6% Prosecco e +9% Asti Spumante), mentre faticano i vini fermi imbottigliati (-3% volume), con i rossi in sofferenza che chiudono a -4% volume e +4% valore, contro il +12% dei bianchi. In particolare, sui rossi, risultano in contrazione i volumi nelle fasce di posizionamento più basse (sotto i 3 euro), mentre tengono molto bene e anzi risultano in buona crescita i vini premium, in particolare piemontesi (+9%), veneti (+4%) e toscani (+6%). I frizzanti cedono il 7% in volume ma guadagnano il 6% a valore.

REGIONI Per quanto riguarda la classifica regionale, con oltre 2,8 miliardi di euro di fatturato all’estero e una performance nei dodici mesi superiore alla media italiana (+13,4%) il Veneto rafforza la sua leadership sulle esportazioni tricolore, guadagnando una quota pari al 36% sul totale nazionale. Si confermano anche il secondo e terzo posto del podio, con il Piemonte in crescita rallentata (+4,6%, a 1,28 miliardi di euro) e tallonato dalla Toscana, che chiude in linea con i risultati nazionali (+10,4%, 1,25 miliardi di euro). A seguire le 3 regioni, responsabili complessivamente del 68,2% dell’export enologico made in Italy, il Trentino Alto-Adige (-1,1% il risultato tra gennaio e dicembre 2022) e l’Emilia-Romagna (+8,9%). Sul fronte delle performance nelle principali regioni enologiche, spiccano le accelerazioni di Friuli-Venezia Giulia (+39,7%), Marche (+25,9%) e Sicilia (+21%). in data:15/03/2023 |

Italia | Mercados | Mundial | Vitivinícola | Jueves, 16 Marzo 2023 | |

| Organic tomatoes in Italy: what prospects after remarkable growth? | Market demand and the reduction of conversion time to organic practices have led to an increase in the surface areas planted with organic tomatoes, but a greater vulnerability of production and increasing inflationary pressure on consumption could slow down this sector.From the article published in L'Informatore Agrario n.6/2023 "Organic tomatoes, what prospects after growth?", by Gabriele Canali and Gloria Zini.The remarkable development of organic food production in recent years has included processed tomato products. The data for northern Italy collected by the Pomodoro IO for this part of the country clearly demonstrates this. Until 2015, surface areas planted with organic tomatoes in northern Italy varied between 1,000 and 1,300 ha, with a share of total areas dedicated to processing tomatoes of about 3% to 4%. These crops really took off after 2016: from 1,309 hectares cultivated organically in 2015, the trend continued to increase to 4,077 hectares in 2022. The same has been true for the share of organic in the total cultivated surface areas in northern Italy, which rose from 3-4% in 2015 to 11% in 2022. |

Italia | Producción | Mercados | Conservas Vegetales | Lunes, 13 Marzo 2023 | |

| Conserve di pomodoro biologico, consumo interno in calo del 6% | AgronewsConserve di pomodoro biologico, consumo interno in calo del 6%Anicav, il 75% del prodotto è destinato all'estero

Roma- Nel 2022 il peso delle vendite nel mercato interno di conserve di pomodoro bio sul totale dei derivati è stato del 4.6% in valore e del 3.2% in volume. I consumi, in Italia, hanno subito un calo del 6% in termini di volumi. Riduzione minore se facciamo riferimento al valore, con una decrescita meno accentuata, ma che comunque registra un -2%. A tenere saldi i conti ci pensa ancora una volta l’export: il 75% dei derivati bio è destinato all’estero e rappresenta il 9,6% del totale esportato. Il comparto delle conserve rosse si conferma, dunque, fortemente export oriented anche per quanto riguarda la produzione certificata bio. Al calo nei consumi interni si contrappone una leggera crescita rispetto al 2021, sia nella produzione che nella quantità di ettari messi a coltura. Durante la campagna di trasformazione 2022 sono state prodotte circa 458.000 tonnellate di conserve bio (circa l’8% del totale) su una superfice di 6.524 ha. Analizzando le differenze tra i due principali bacini si registra una produzione maggiore al nord con circa 266.000 tonnellate di prodotto trasformate (poco più del 9% del totale), rispetto alle 192.000 provenienti dal centro sud (7,4% del totale). Sono questi i principali dati emersi dall’indagine conoscitiva sul pomodoro biologico passato alla trasformazione nel 2022, condotta da Anicav Associazione Nazionale Industriali Conserve Alimentari e Vegetali. “Le conserve di pomodoro biologico giocano un ruolo sicuramente di primaria importanza per il nostro comparto. – dichiara Giovanni De Angelis, Direttore Generale di Anicav – A conferma di ciò nell’ultimo quinquennio, per rispondere alle esigenze di un consumatore sempre più attento alla qualità dei prodotti e alla tutela dell’ambiente, si è registrata una crescita del 66,5% degli ettari messi a coltura e del 65,70% delle quantità trasformate di pomodoro bio. Il calo dei consumi interni nell’ultimo anno è certamente da addebitare alle crescenti difficoltà economiche dei consumatori che, tra inflazione e caro bollette, hanno ridotto gli acquisti di un prodotto con un prezzo più caro rispetto al convenzionale. In aiuto, sicuramente, l’export che compensa quanto perduto sui mercati interni. Ora guardiamo alla prossima campagna, monitorando con grande attenzione le criticità con cui dovremo certamente fare i conti, dalla siccità all’andamento dei costi di tutte le materie prime”. in data:10/03/2023 |

Italia | Mercados | Clientes | Conservas Vegetales | Jueves, 09 Marzo 2023 | |

| Starbucks Introduces Olive Oil-Infused Coffee in Italy |

A new line of cold coffee beverages is made with Sicilian extra virgin olive oil.  By Daniel Dawson Feb. 22, 2023 15:30 UTC Starbucks has presented a new line of olive oil-infused coffee at its locations across Italy. The company plans to introduce the beverage in California in the spring and the United Kingdom, Japan and the Middle East later in the year. Howard Schultz, the company’s interim chief executive, said five new hot and cold brewed beverages would be made with Nocellara del Belice extra virgin olive oil sourced from Partanna, Sicily. I was absolutely stunned at the unique flavor and texture created when the Partanna extra virgin olive oil was infused into Starbucks coffee.- Howard Schultz, interim CEO, Starbucks The Brooklyn native said the inspiration for the new olive oil coffee line came after a trip to Sicily. He was introduced to the custom of drinking a tablespoon of extra virgin olive oil before his morning coffee. Soon after, he started mixing the olive oil with the coffee. “I was absolutely stunned at the unique flavor and texture created when the Partanna extra virgin olive oil was infused into Starbucks coffee,” Schultz said. “In both hot and cold coffee beverages, what it produced was an unexpected, velvety, buttery flavor that enhanced the coffee and lingers beautifully on the palate.” See Also:How to Mix the Perfect EVOO CocktailsAmy Dilger, the company’s principal beverage designer, was charged with creating the new olive oil-infused drinks. After researching extra virgin olive oil, she blended the oil with the company’s blonde espresso roast, which the company describes as having “smooth, well-rounded flavors that are delicious both hot and iced.” Italy is Europe’s third-largest coffee market, with an annual per capita consumption of 5.3 kilograms. However, there has long been plenty of antipathy toward Starbucks. In 2018, Starbucks announced plans to open its first store in Milan, the country’s second-largest city and economic hub. In protest, Italians set fire to some of the palm trees in the Piazza del Duomo, an iconic city landmark where the first store was set to open. Eventually, there was a gradual acceptance of the chain. The decision to launch an olive oil-based line of coffee comes after a flurry of other olive and olive oil beverage infusions. Last March, an entrepreneur in Liguria, a region of northern Italy, launched an olive oil-infused vodka. Like Schultz, he said adding olive oil gave the vodka a velvety texture. In Spain and Italy, two separate companies recently introduced olive-infused beer. Producers in Lazio added olive leaves obtained from pruning to the traditional brewing process, resulting in a smoky taste in the beer. Meanwhile, an award-winning Spanish beer uses Empeltre olive extract, which infuses the flavors, aromas and colors of the olives into the beer. While all three of these products have won regional and international acclaim, it remains to be seen how Italy’s coffee-enthusiastic public takes to the new drinks. Advertisement Related Articles |

Mundial | Mercados | Otros | Italia | Producción | Aceite | Martes, 21 Febrero 2023 | |

| Analisi della catena del valore della filiera olio di oliva | [unable to retrieve full-text content]Analisi della catena del valore della filiera olio di oliva -- Delivered by Feed43 service |

Italia | Mercados | Miércoles, 08 Febrero 2023 | |

| La logistica integrata a valle nella filiera biologica italiana del pomodoro da industria | [unable to retrieve full-text content]La logistica integrata a valle nella filiera biologica italiana del pomodoro da industria -- Delivered by Feed43 service |

Italia | Mercados | Miércoles, 08 Febrero 2023 | |

| Vino: Uiv-Vinitaly, 2022 in flessione per i vini tricolore in Usa, Germania e Uk | AgronewsVino: Uiv-Vinitaly, 2022 in flessione per i vini tricolore in Usa, Germania e UkNei tre top buyer lo scorso anno sono stati venduti 4,9 milioni di ettolitri di vino, equivalenti a un calo del 9% rispetto al 2021

Roma- Bilancio 2022 negativo per il vino italiano nel circuito retail e Grande distribuzione di Usa, UK e Germania, che da soli valgono circa il 50% delle esportazioni italiane. Nei tre top buyer, secondo i dati elaborati dall’Osservatorio del Vino Uiv-Vinitaly su base Nielsen-Iq, lo scorso anno sono stati venduti 4,9 milioni di ettolitri di vino, equivalenti a un calo del 9% rispetto al 2021, per valori in riduzione del 5%, a 4,7 miliardi di euro. Rispetto alle vendite del 2021, manca all’appello l’equivalente di 63 milioni di bottiglie e un controvalore di 253 milioni di euro. Fra i tre mercati, le performance generali peggiori si registrano in UK (-11% volume e -8% valore), mentre gli Usa smorzano a -2% l’erosione in valore (2,1 miliardi di euro), limitando il minus a volume a -5%. La Germania al -7% valoriale affianca una perdita del 10% volume (1,7 milioni di ettolitri). Il bicchiere è però mezzo pieno, rileva l’Osservatorio, se si considera che alla dinamica discendente sul canale della grande distribuzione corrisponde la riapertura del fuori casa, con un mercato della ristorazione dato in crescita consistente. In sintesi, un ritorno alle normalità del pre-Covid, crisi economica permettendo. In tutti e tre i mercati, per diverse denominazioni si riscontra infatti un ritorno più o meno soft ai livelli del 2019, con il Prosecco che gioca una partita a parte, con incrementi in doppia cifra sul periodo.

Nell’ultimo anno, forti erosioni dei volumi venduti negli Usa per Chianti (-9%), Lambrusco (-13%), Montepulciano d’Abruzzo (-12%), e Rossi piemontesi (escluso Barolo, -10%), mentre prosegue in scia positiva la corsa del Prosecco, a +4% (+41% sul 2019) e sul versante Rossi cresce del 5% il Brunello di Montalcino. In Germania, situazione complicata per il Primitivo (-8%) e contrazioni volumiche in doppia cifra per Pinot Grigio e Nero d’Avola, oltre a Lambrusco e Prosecco (-14,5%) in data:06/02/2023 |

Italia | Mercados | Competidores | Vitivinícola | Alemania | EEUU | Reino Unido | Lunes, 06 Febrero 2023 | |

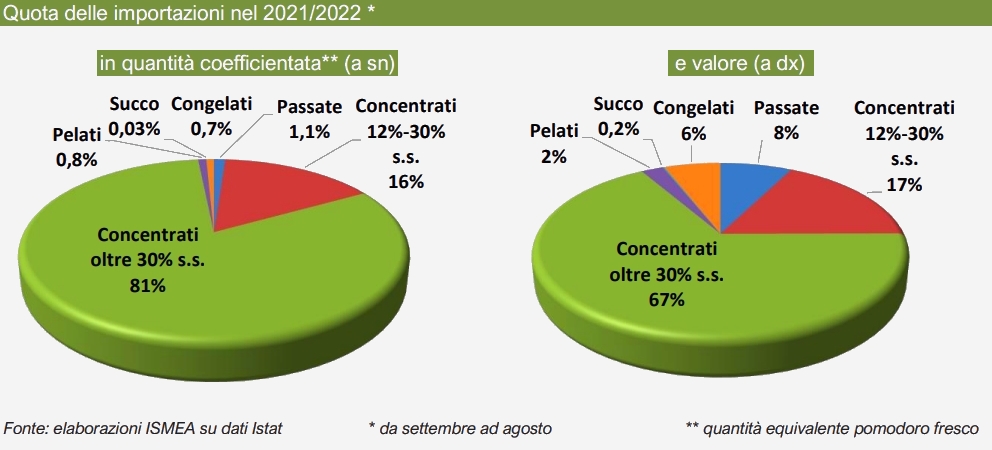

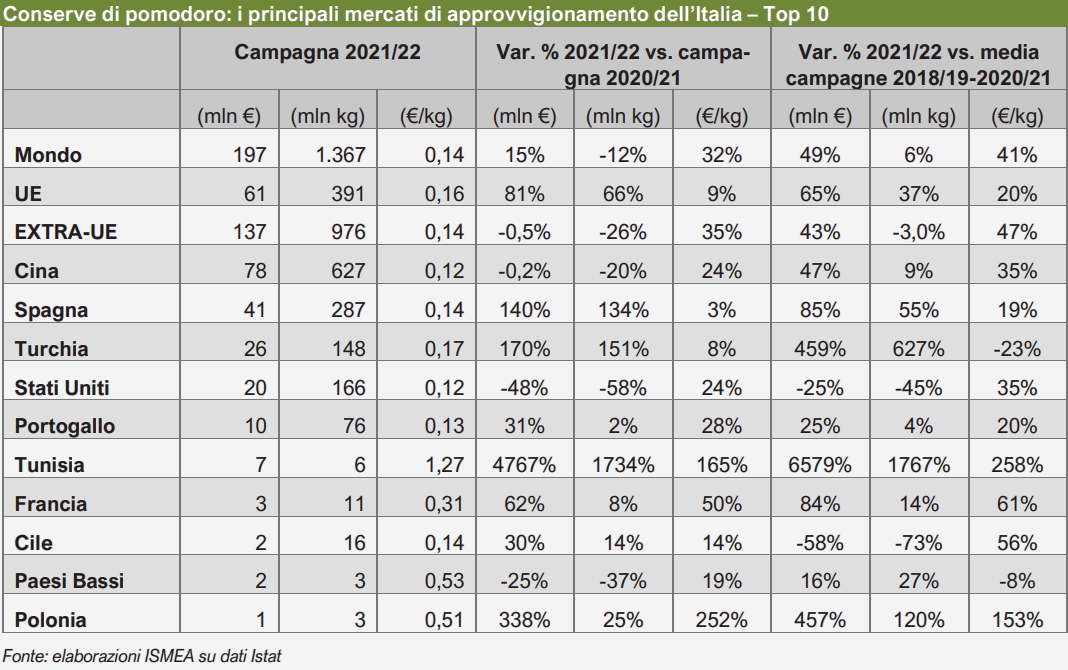

| Publication: ISMEA, focus on processing tomatoes in Italy |

The situation as it stands

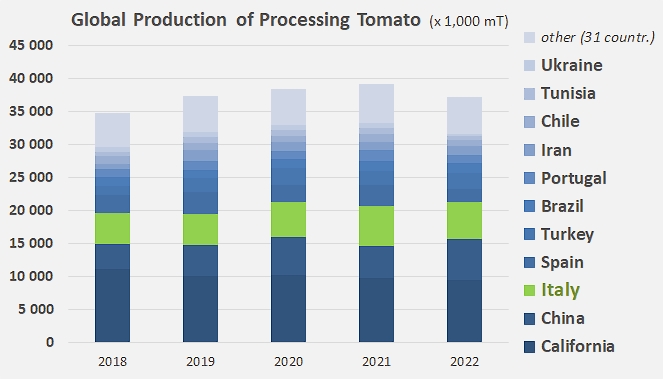

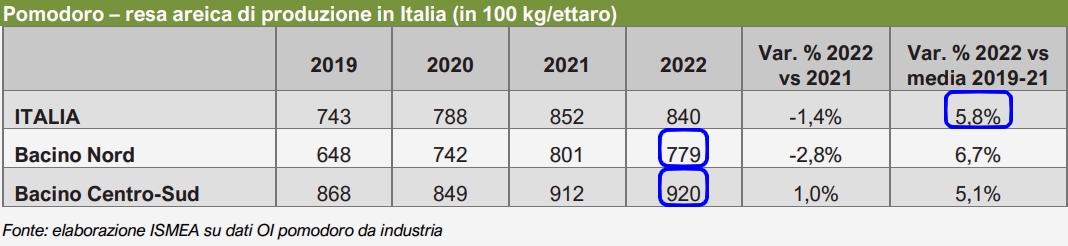

According to a report published last December by ISMEA, Italy is the third largest producer of tomatoes for processing in the world. In 2022, about 5.5 million tonnes of tomatoes were produced and processed in the country, which is about 15% of the world's production and 56% of the European crop. According to a report published last December by ISMEA, Italy is the third largest producer of tomatoes for processing in the world. In 2022, about 5.5 million tonnes of tomatoes were produced and processed in the country, which is about 15% of the world's production and 56% of the European crop.The industrial turnover of this sector exceeds EUR 4 billion, of which exports account for 2.2%. The ISMEA report also confirms that Italy is the leading producer of canned tomatoes destined directly for final consumers and that 60% of Italian processed products are exported. These items of information highlight Italy's leading role at the global level and therefore the importance of this sector within the national agri-food industry.

The raw material market is characterized by prices defined in the framework of interbranch agreements and therefore the price is determined in each of the two production basins, for each of the types of products (round fruit, oblong fruit and cherry tomatoes). However, a comparison of 2022 prices with previous years shows an increase in reference prices.

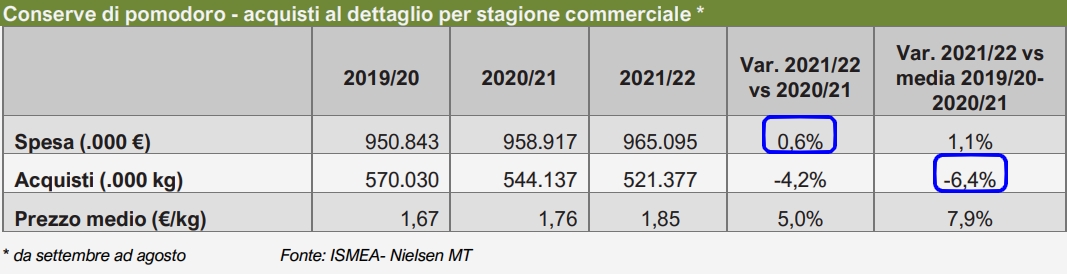

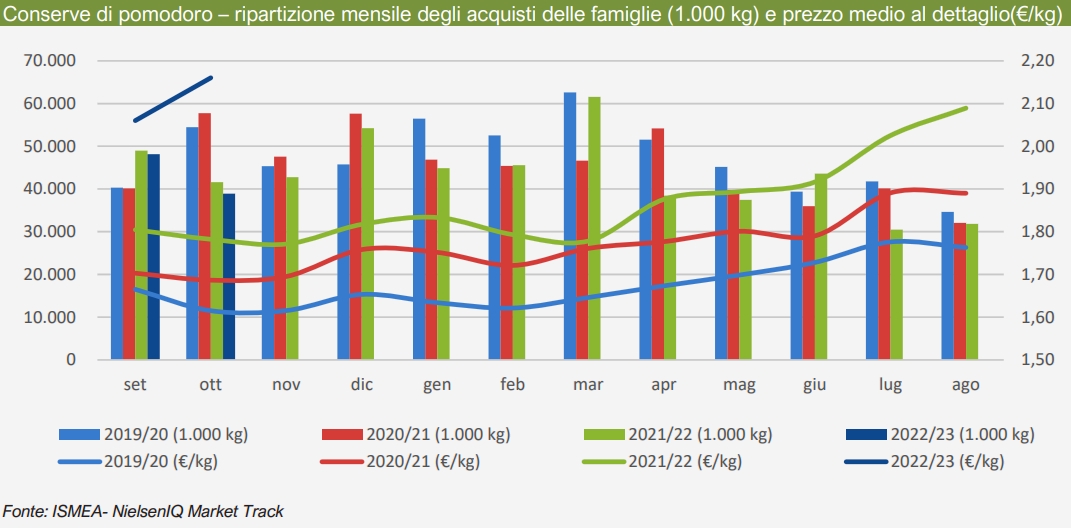

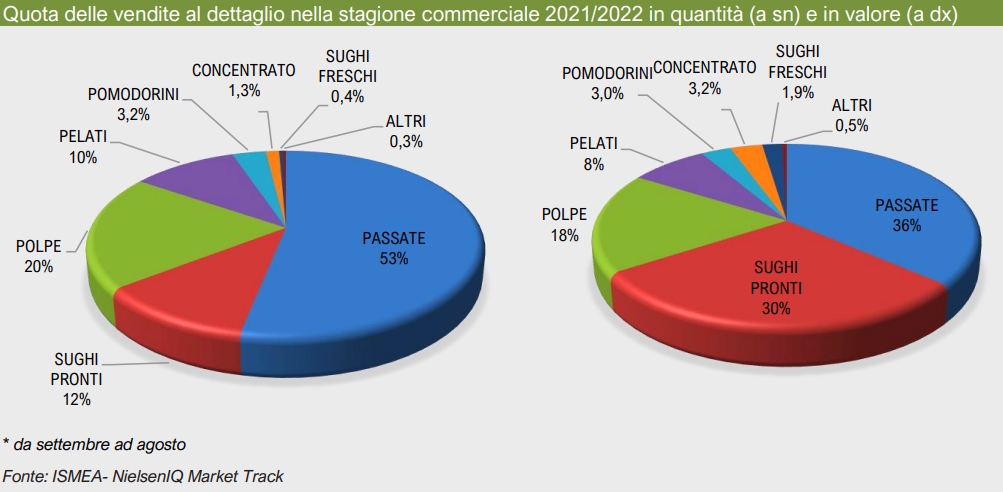

Retail sales

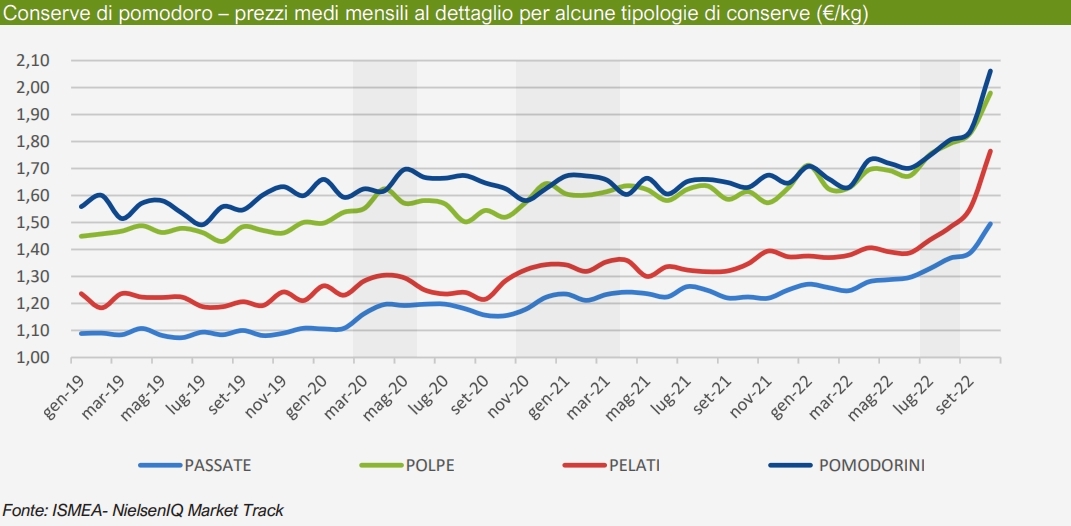

The market for canned tomatoes features a basic pattern of gradual reduction in quantities due to the decrease in the number of meals at home, the reduction in time spent preparing meals and the replacement of red condiments by other types of condiments. The contraction of the quantities sold is counterbalanced by an increase in spending, which is based on two different mechanisms. On the one hand, there is an increase in average prices which affects all tomato product references. On the other hand, a dynamic has been affecting the market for several years now, tending to gradually replace basic products (peeled tomatoes and pulp) in the consumer's basket with products that have a higher service content (ready-to-use purees and sauces).

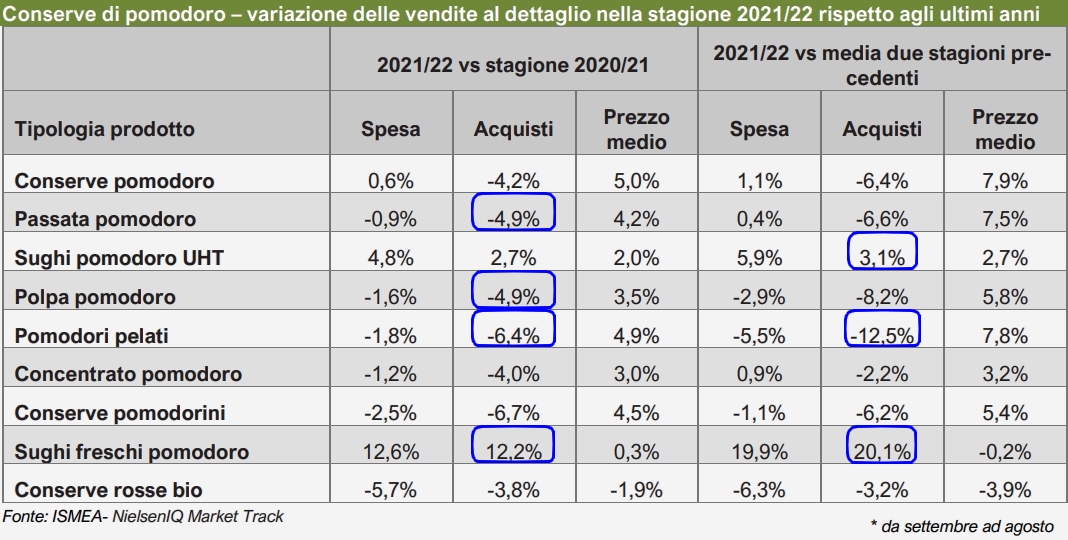

Variations in annual sales recorded for the 2021/2022 marketing year for each product type are summarized in the table below. As the decline affected all the main product references, there was no substantial difference in terms of shares held by the various products compared to previous year records.  Certified organic tomato products in cans now represent about 5% of total retail sales in Italy, with the main product categories being purees, pulps, sauces and to a lesser extent peeled tomatoes. This market segment has proven to be very dynamic in recent years. However, the 2021/2022 campaign has been marked by a slowdown in sales. A comparison with the previous business year shows a slowdown in sales (-3.8%) and a slight fall in average prices (-1.9%), for a segment that was unable to keep up the pace of sales recorded during the pandemic.

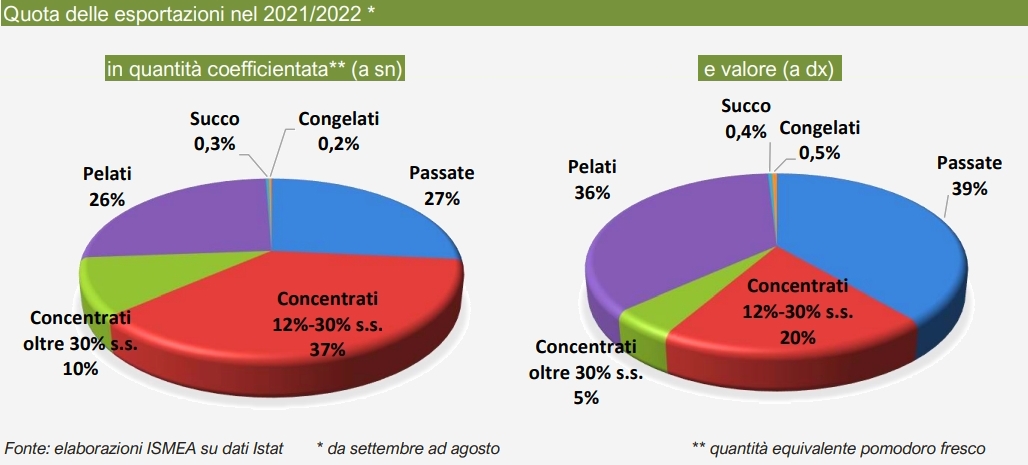

Italy's foreign trade  The comparison of annual performances shows that the last marketing year was characterized by a significant increase in average prices, which rose by 32% for imported products and 11% for exported products. In this regard, it should be noted that Italy imports semi-finished products – mainly tomato paste with more than 30% soluble solids content – at an average price of 14 cents of a euro per kg of raw tomato equivalent, and exports finished products (purees, peels and paste with a soluble solids content of less than 30%) at an average price of 52 cents of a euro per kg of raw tomato equivalent.

In terms of value, the most exported canned tomato products are peeled tomatoes (36%) and purees (39%), which together account for three quarters of exports. The 20% share of tomato paste (12-30% soluble solids) brings this total to more than 95%, the list being completed by the 5% share of pastes with more than 30% soluble solids and by a marginal quantity of less than 1% attributable to tomato juice.

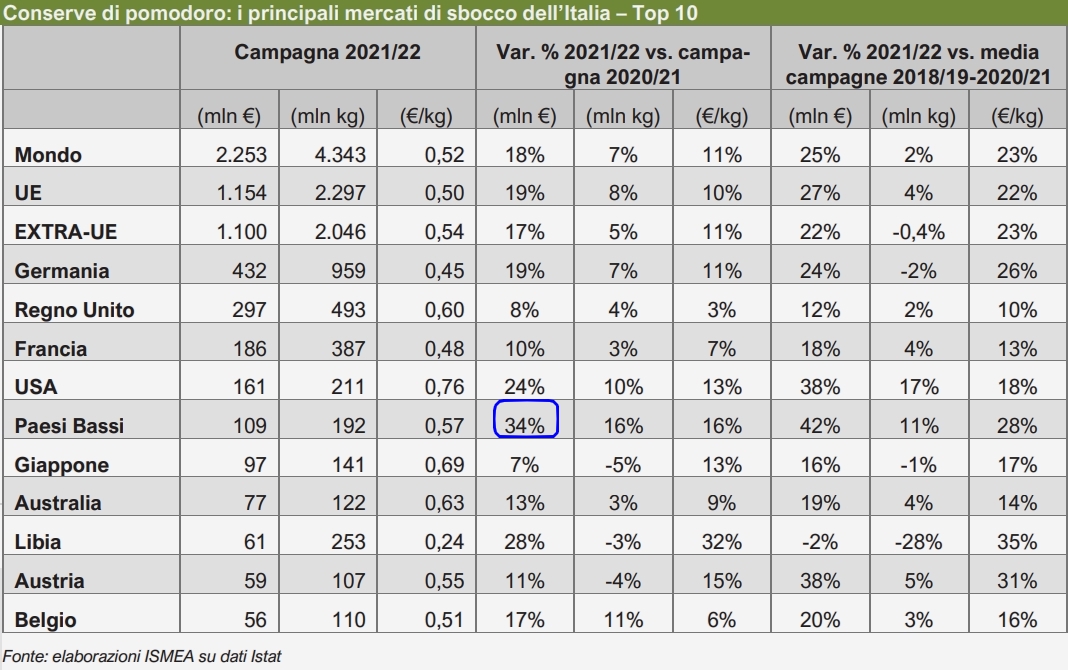

Final considerations Once the processing season is over, the main concerns for the 2022/23 marketing year are the impact on retail prices of rising energy and raw material costs, and the inflationary wave that has hit European households. It is important to emphasize that the prospects of the sector are inextricably linked to the success of canned tomatoes on foreign markets and, in this sense, the news of reduced transportation costs provides a degree of optimism for trade in the coming months.

Some complementary information Sources: ismeamercati.it, corriereortofrutticolo.it |

Italia | Mundial | Mercados | Conservas Vegetales | Producción | Jueves, 02 Febrero 2023 | |

| Cresce il commercio estero extra UE | Con un aumento del 14% è record storico per l’export agroalimentare italiano fuori dall’Unione Europea dove ha raggiunto il valore di 26 miliardi nel 2022, pari a oltre il 43% del totale delle esportazioni. È quanto emerge dalle stime della Coldiretti nel commentare i dati Istat sul commercio estero Extra UE relativi al mese di dicembre. “A spingere il Made in Italy sulle tavole fuori dai confini comunitari è la forte domanda degli Stati Uniti in salita del 20% mentre,” sottolinea la Coldiretti, “si registrano risultati positivi anche nel Regno Unito con un +18% che evidenzia come l’export tricolore si sia rivelato più forte della Brexit, dopo le difficoltà iniziali legate all’uscita dalla UE. Balzo a doppia cifra anche nella Turchia di Erdogan (+23%) mentre è dato negativo in Cina con un calo del 20% e in Russia con un -5% fra sanzioni, guerra e pandemia Covid”. L’export alimentare è trainato dai prodotti simbolo della Dieta Mediterranea come vino, pasta e ortofrutta che salgono sul podio dei prodotti italiani più venduti all’estero. Il successo dei prodotti della Dieta Mediterranea all’estero confermano l’alto gradimento per la cucina italiana che si è classificata come migliore dieta al mondo del 2023 davanti alla dash e alla flexariana secondo il best diets ranking elaborato dal media statunitense U.S. News & World’s Report’s, noto a livello globale per la redazione di classifiche e consigli per i consumatori. “Ma è sotto attacco,” continua la Coldiretti, “del moltiplicarsi delle imitazioni sui mercati esteri, dal parmesan alle mitazioni di Provolone, Gorgonzola, Pecorino Romano, Asiago o Fontina mentre tra i salumi sono clonati i più prestigiosi, dal Parma al San Daniele, ma anche la mortadella Bologna o il salame cacciatore e gli extravergine di oliva o le conserve come il pomodoro San Marzano”. C’è anche il rischio di un nuovo protezionismo alimentato da etichette ingannevoli come quelle a colori, un sistema di etichettatura fuorviante, discriminatorio ed incompleto che finisce paradossalmente per escludere dalla dieta alimenti sani e naturali che da secoli sono presenti sulle tavole per favorire prodotti artificiali di cui in alcuni casi non è nota neanche la ricetta. I sistemi allarmistici di etichettatura a semaforo si concentrano esclusivamente su un numero molto limitato di sostanze nutritive (ad esempio zucchero, grassi e sale) e sull’assunzione di energia senza tenere conto delle porzioni, escludendo paradossalmente dalla dieta ben l’85% in valore del Made in Italy a denominazione di origine. “Per sostenere il trend di crescita dell’enogastronomia nazionale serve ora agire sui ritardi strutturali dell’Italia e sbloccare tutte le infrastrutture che migliorerebbero i collegamenti tra Sud e Nord del Paese, ma anche con il resto del mondo per via marittima e ferroviaria in alta velocità, con una rete di snodi composta da aeroporti, treni e cargo,” afferma il Presidente della Coldiretti Ettore Prandini nel sottolineare l’importanza di cogliere l’opportunità del PNRR per modernizzare la logistica nazionale che ogni anno rappresenta per il nostro Paese un danno in termini di minor opportunità di export. Ma è importante lavorare anche sull’internazionalizzazione per sostenere le imprese che vogliono conquistare nuovi mercati e rafforzare quelli consolidati valorizzando il ruolo strategico dell’Ice con il sostegno delle ambasciate.

Fonte: coldiretti.it  |

Italia | Mercados | Intersectorial | Lunes, 30 Enero 2023 | |

| Pomodoro da industria, questanno al Centro-Sud serve unintesa più veloce e condivisa sul prezzo |  È la richiesta di Cia Agricoltori Italiani di Capitanata, memore del grosso ritardo nella firma del contratto nel 2022 e delle sue ripercussioni su superficie, produzione e prezzi. Intanto è stato avviato il percorso che condurrà al riconoscimento della Dop Pomodoro pelato di Puglia Quest’anno bisogna trovare subito un’intesa sul prezzo del pomodoro da industria agli agricoltori del Centro-Sud, per evitare quanto accaduto nel 2022, quando si sono coltivati 2.000 ettari in meno rispetto al 2021, concentrati quasi tutti nel Foggiano, una perdita netta di circa tre milioni d quintali. La richiesta, che è anche un monito, arriva da Angelo Miano, presidente di Cia Agricoltori Italiani di Capitanata. «Ora è il momento di dare ai produttori una base minima di certezze per metterli nelle condizioni di programmare e di trapiantare. Nella campagna del pomodoro 2022 l’intesa sul prezzo fu raggiunta solo a luglio. Troppo tardi poiché, in assenza di accordo, molte aziende agricole decisero in primavera di non procedere con i trapianti». Pomodoro da industria, nel 2022 tardi accordo sul prezzo

I numeri, rileva Miano, dimostrano le conseguenze dell’accordo tardivo: nel 2022 in Capitanata sono sati raccolti circa 12 milioni di quintali di pomodoro, a fronte dei 14.782.000 del 2021. In calo anche le superfici coltivate: il pomodoro coprì nel 2021 17.140 ettari, mentre nel 2022 si è scesi a 15.000 (sui 32.500 in Italia). «L’anno scorso le industrie conserviere hanno tirato la corda al massimo pur di non riconoscere un valore adeguato da corrispondere ai produttori. Il calo delle superfici coltivate e, di conseguenza, la minore produzione sono state la diretta conseguenza delle politiche attuate da parte industriale. Abbiamo penato per mesi prima di poter arrivare a un accordo sul prezzo del pomodoro da industria. Un’incertezza durata diversi mesi, tanto da spingere molti imprenditori agricoli a rompere gli indugi e rinunciare a trapiantare». Nel 2022 alla fine il prezzo l’ha fatto il mercatoL’accordo fu raggiunto nei primi giorni di luglio, con un’intesa basata su 13 centesimi al chilo per il pomodoro tondo, 14 centesimi al chilo per il lungo e una maggiorazione del 30% per il prodotto biologico. A fine campagna, però, il tondo raggiunse i 16 centesimi al chilo e il lungo, per il pelato, 21 centesimi. «Una piena dimostrazione – sostiene Miano – di quanto poco assennate siano state le scelte della parte industriale, arroccata su quotazioni insufficienti anche a coprire i costi di produzione per le aziende agricole, ma poi costretta a subire le conseguenze delle sue stesse azioni con la riduzione delle superfici coltivate e la conseguente corsa all’accaparramento del prodotto in campo, che hanno fatto aumentare i prezzi ben oltre le richieste iniziali degli agricoltori». Le industrie riconoscano un prezzo remunerativoPer Cia Agricoltori Italiani di Capitanata, dunque, se c’è la volontà, nel 2023 si può fare molto meglio. Occorre, tuttavia, che le industrie conserviere arrivino molto prima a riconoscere un prezzo remunerativo al pomodoro prodotto in provincia di Foggia. «È necessario che la parte industriale sia guidata da visioni più ampie, capaci di considerare l’interesse dell’intera filiera. Si tornerà ai numeri del 2021 solo e soltanto se ci sarà un cambiamento da questo punto di vista, rompendo il muro creato da egoismi di parte che poi si rivelano autolesionistici, come dimostra il bilancio dell’ultima stagione del pomodoro». Partito iter per Dop Pomodoro pelato di PugliaIntanto, con la presentazione del disciplinare di produzione, è stato avviato il percorso che condurrà al riconoscimento della Dop Pomodoro pelato di Puglia. «La Dop per il pomodoro di Puglia, che Cia Capitanata chiedeva da tempo, è un primo e importante passo per rilanciare una filiera che, in provincia di Foggia, rappresenta un’eccellenza assoluta per quantità e qualità. Abbiamo collaborato alla redazione del disciplinare e questo percorso ci vede assolutamente partecipi e convinti dei passi che andranno svolti da qui in avanti, il primo dei quali resta un’intesa soddisfacente e giusta sul prezzo del pomodoro da corrispondere ai produttori nella campagna 2023 |

Italia | Mercados | Conservas Vegetales | Martes, 24 Enero 2023 |

Página 1 de 33